Modern Slavery in Private Markets: From statements to meeting supply chain management expectations

by Dean Alborough

View post

Technical Director, Bob Robinson and Principal Environmental & Social Specialist, Zhanar Faizuldaeva recently presented at the Organisation for Economic Co‑operation and Development (OECD) high‑level workshop in Kazakhstan. This also marked the launch of an OECD publication on Advancing Security and Transparency for Critical Raw Materials (CRMs) Governance in Central Asia.

Greenhouse Gas commitments for countries in Central Asia are outlined in nationally determined contribution statements. These are required for all countries within the Paris Agreement, and each country must include a plan to reduce greenhouse gas emissions to help meet the global goal of limiting temperature rise to 1.5ºC. These have been considered for Kazakhstan, Uzbekistan, Kyrgyz Republic and Tajikistan and key points are shown below:

For all countries, route maps and specific measures for industry are needed, in particular for the mining and metals sectors.

There are several significant drivers for industry to decarbonise:

Attract finance: Major international financers favour companies taking significant measures to decarbonise.

Legislation: Legislation could support decarbonisation, however, at the moment this is lacking in countries in central Asia. Much of the production of metals and mining flows into the EU and other regulated markets. The Carbon Border Adjustment Mechanism (CBAM) favours products with lower carbon intensity.

Grid constraints: In remote areas, grid constraints can be a major concern therefore, decarbonisation through installation of renewable energy would reduce reliance on energy from the grid.

Customer demands: Many customers are also concerned with their carbon footprint, which includes suppliers, and therefore they may select their suppliers based on the carbon intensity of the product.

Save money: Decarbonisation through energy efficiency can result in a reduction in operational costs however, some measures (such as heat pumps and carbon capture) can result in an increase in operational costs initially but may have a long-term financial benefit.

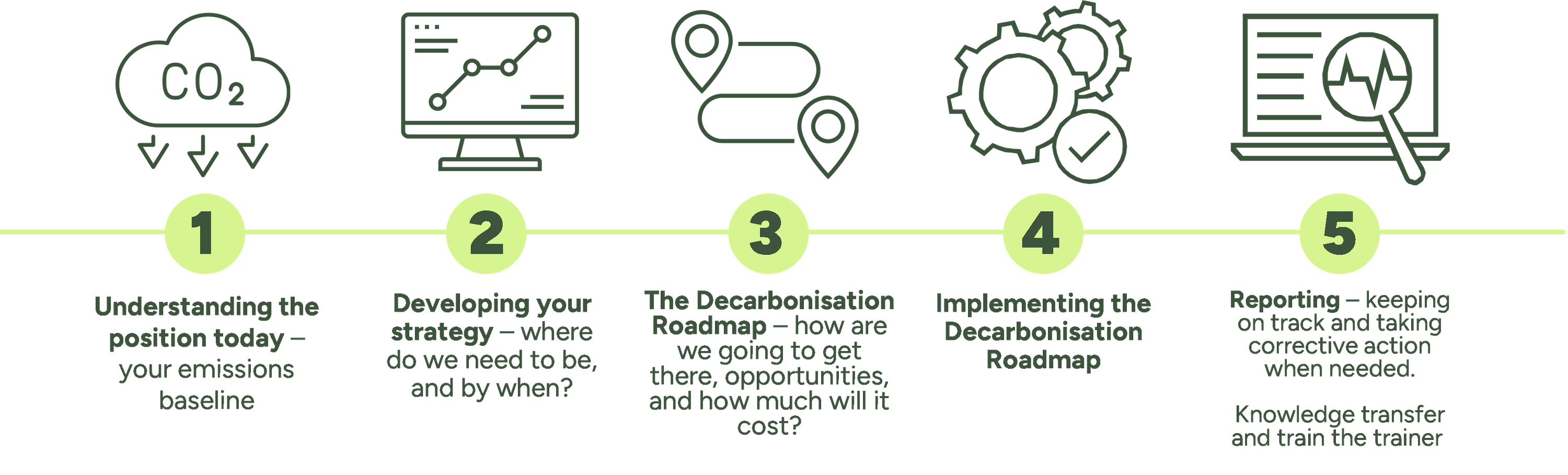

In order for mining and metals companies to decarbonise, a five step strategy is recommended.

Step 1 - Understand the position today: Calculate your emissions baseline which should include Scope 1, 2 and 3. Scope 1 includes direct energy consumption (such as natural gas, diesel, oil, etc.) and process emissions. Scope 2 are those associated with imported energy, such as grid electricity. Scope 3 emissions are those associated with upstream and downstream supply chains, emissions from third parties eg: equipment suppliers 3rd party transport and distribution.

Step 2 - Developing your strategy: Once the data is in place for the carbon footprint, a strategy should be developed, including setting targets for carbon reduction. Some large mining companies have been set individual reduction targets by governments. This can be supported by a public commitment. Examples of declarations and commitments include:

Step 3 - Decarbonisation roadmap: A decarbonisation roadmap includes a practical plan for implementation of measures which will allow the organisation to meet their targets. There is an interdependency between carbon, energy, water, waste, circular economy, process efficiency. It is recommended that a decarbonisation roadmap consider all of these aspects together, so as to develop the most cost effective and business centric plan.

The decarbonisation roadmap needs to be dynamic, taking into account mineral quality, energy and water costs, quality, transport and customer specifications.

The availability and maturity of available technology will also impact the plan. Proven technology provides lower risk and more certain outcomes and benefits.

Step 4 - Implementing the decarbonisation roadmap: Implementation must be planned carefully to take into account finance availability, project lead times, product demands.

Step 5 - Reporting: Continuously monitoring the decarbonisation impact will enable quantification of benefits and ensures savings are maintained. Monitoring will also indicate where operating practices are diverting from the optimum or if equipment efficiencies are reducing. A metering and verification strategy should be included with every project before implementation.

Any reporting should be verified as being robust and correct for external publication.

The CRM sector includes all operations for deep and open cast mining to ore preparation and metals production. Key areas for decarbonisation and carbon management for the CRM sector include:

How could these be mitigated: It is possible to look at each area for decarbonisation in isolation, however this would not result in an optimal solution and is likely to require higher CAPEX. There are however several techniques than can be applied to the whole value chain:

Are there any case studies or interesting projects?

Global mining and minerals company conducted integrated efficiency programme, using external and internal resources. Global dashboards and benchmarking of achieved savings helped track and motivate further savings. An internal cost of carbon supported prioritising decarbonisation projects. The project achieved incremental savings of US$10-14M every year over more than 10 years.

Modelling of mining and metals production in South America enabled clarity of investment strategy and robust decisions to be made. Over 200 mitigation measures were modelled over life of mine, taking into consideration mineral quality, energy and water availability and costs and carbon emissions.

For more detail is available on how to decarbonise, with many calculation tools and industrial specialists.

Get in touch

by Dean Alborough

by Bob Robinson

by Genevieve Sew, Shan Min Tan, James Balik-Meacher